4 Common Misconceptions in Planning for Retirement

Think you’re on track for retirement by contributing monthly to your savings? Think again. When it comes to a secure retirement, just contributing to your monthly savings may not be enough. Calculating goals, reevaluating strategies and adjusting contributions are just as essential as lifestyle changes before and during retirement.

Here are 4 of the most common misconceptions people have when planning for retirement:

- There’s more than enough time to save.

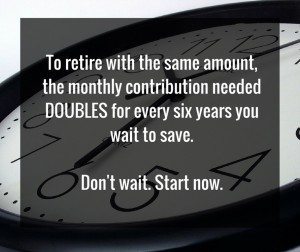

You may believe you’ll work forever and have time to save, but often that isn’t the case. Many Americans are focused on paying down student loans and other debt, or concentrating on more immediate goals like buying a house and children’s college funds. However, putting off retirement savings will add up. The monthly amount you need to set aside to reach the same level of retirement income doubles for every six years you wait to start saving.

It’s not only what you contribute, but the time it takes to grow that is important. Over time, the savings really add up!

- Contributing regularly to retirement savings is the same as a savings plan.

Adding steadily to retirement savings is a great start, but make sure your savings aren’t on autopilot. The Employee Benefit Research Institute found 39% percent of people guess how much they will need to save without actually calculating their needs in retirement.

Take the time to calculate your needs and set a strategy to achieve measurable financial goals. Make sure to plan for a cushion–Americans are living longer, accumulating more healthcare costs as they age and as costs rise.

- When saving steadily there’s no need to update your savings strategy.

Volatility in the stock market can affect your savings – as does your current expenses and future needs. Career changes and family situations can also change how you should be saving. Leading up to retirement, your last few years of savings will be different than when you were first starting out in your career. Even once you start your retirement, it’s beneficial to review your strategy.

Revisit your retirement plan every few years to make sure your savings reflect your needs and adjust for market conditions. Diversifying your portfolio to include low risk products like fixed indexed annuities can also help moderate risk through shifts in the market.

- Focusing on one retirement savings account is a safe option.

A report from the Economic Policy Institute found a shift from pension funds to retirement accounts with employees in the driver’s seat. The responsibility to choose strategies and mitigate risks while saving for retirement is now mostly falling to the employee. Savers should protect themselves from market risk and protect the value of their nest egg while maintaining a varied portfolio. The level of risk should reflect your age and goals.

For example, younger savers have more time to recover from risk than those nearing retirement. One option to provide balance to your retirement portfolio is a Fixed Indexed Annuity (FIA), which protects your principal and can provide a guaranteed stream of income in retirement.